On Friday night I published a deep dive into Dalhousie University’s finances. While it was a long post, it was limited to trying to explain the university’s financial situation in light of a clear explanation of how the budget works. It left open a few questions about the university’s budgeting policy and budgeting decisions. Here’s the most important one.

In my calculations of how the university paid for its consolidated surpluses over the last ten years, one aspect of my calculations has continued to bother me. Some of the increase came from operational surpluses and carry-forwards, but the big part came from capital investment. I needed to explain not only the $349 million increase in the capital fund, but also how the university defrayed $446 million in capital depreciation. I concluded that these funds came primarily from four sources: $331 million from operational spending for campus renewal, $167 million from gifts and grants, $131 million out of capital contributions from ancillary services including rent from student housing, and $77 million from income within the capital fund itself.

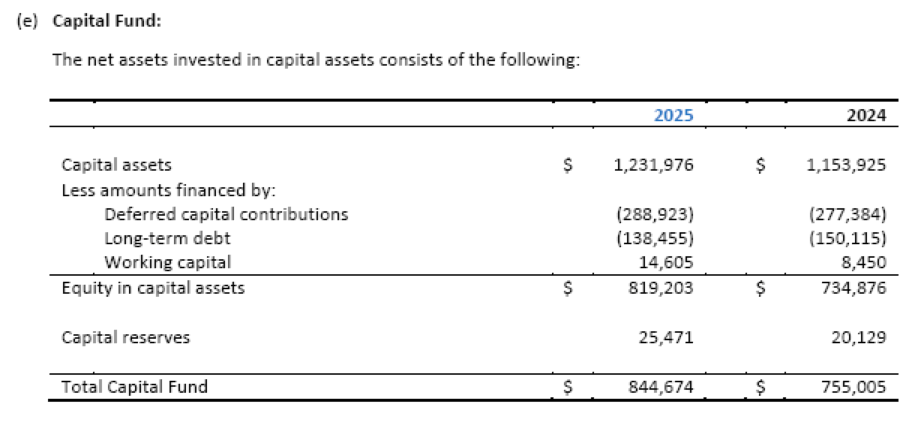

It’s that $77 million I’ve been worrying over. As a collection of assets, the fund accounts for the value of physical assets, net of debt and deferred capital contributions. In terms of revenue and expenses, it’s a cost centre. It accounts for interest paid on capital projects and the deprecation of capital goods. Those costs are paid for by donations and transfers from other funds. It is not supposed to have any meaningful revenue of its own. Here’s a snapshot of the fund from last year.

Now, there is one way that the capital fund could be said to earn money. As seen above, the capital fund includes a small capital reserve, described in financial statements as “funds set aside by the University for the costs of large-scale capital upgrades or replacements planned for the future.” Capital reserves have increased from about $11 million in March 2015 to $25 million in March 2025.

Insofar as these are assets designated as belonging to the capital fund, it is reasonable that the university would also attribute some proportion of its overall investment income to the capital fund. If invested assets earn 5-7% per year, the university might reasonably count 5-7% of the capital reserves as investment income within the capital fund.

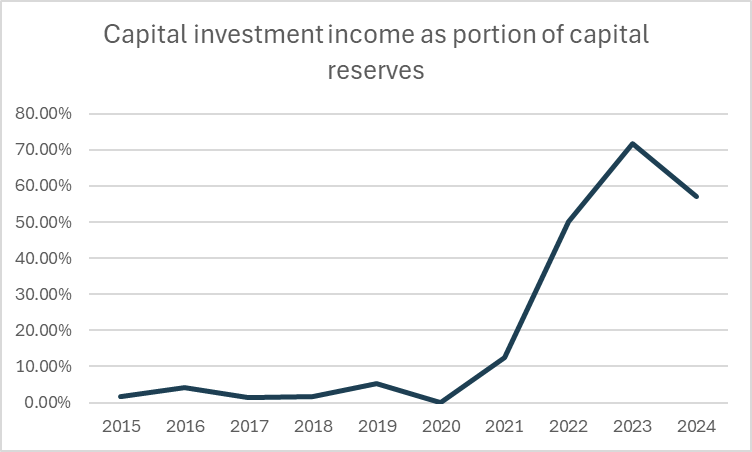

The problem is that the investment income “earned” in the capital fund or, more precisely, the investment income that the (unaudited) schedules to the financial statements designate as revenue earned in the capital fund, bears no consistent relationship to capital reserves over the last ten years. As shown below, designated “capital investment income” was 70% of capital reserves in 2023-24.

Why does this matter? In my break down last week, I argued there are basically two links between the university’s operating budget and its capital budget, which was key in turn to articulating how the university can have a consolidated surplus, even when the operational budget is in deficit. First, at least once in the last ten years, the board allocated $300 000 from the operating budget to “capital investment” on new infrastructure. (Apparently, they also spent part of an operating surplus on new infrastructure in 2022, including on the new arena). The other link I pointed to are funds allocated in the operational budget every year for “campus renewal.”

After reading my post, Dan Cohen, who has been active working on faculty budget activism at Queens, pointed out a third possible link between the operational budget and capital spending. Namely, a university might (and apparently Queens did) reallocate investment income to the capital fund rather than to the operating fund. The result would be less investment income to spend on operations, lower operational surpluses (or worse deficits), and a corresponding increase in the consolidated surplus, in line with the additional resources allocated to the capital fund.

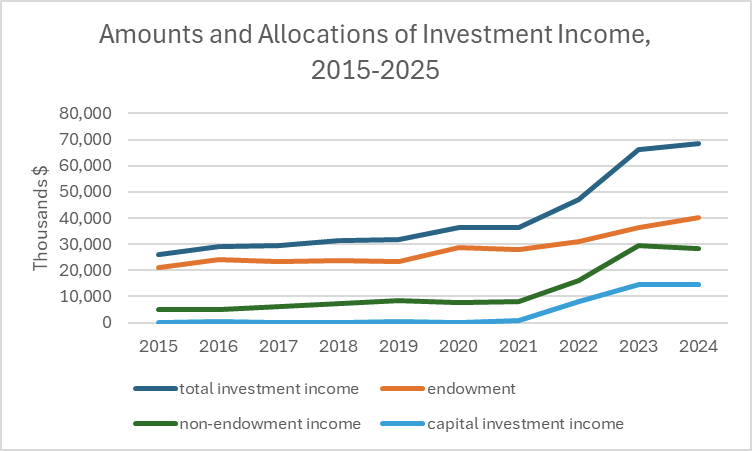

Is this something that has been happening at Dalhousie? Based on the data that I have, it certainly appears to be. Here are the basic facts. As shown in the graph below, total investment income grew gradually between 2015 and 2021, and then jumped radically over the last four years. Recent annual financial reports attribute this jump to a rise in interest rates that has allowed the university to earn more from GICs and similar instruments. Between the 2015 and 2024 fiscal years, total investment income increased from $26 million to about $69 million. Much of that income is earned within the endowment, but as total investment income has grown, so has the proportion earned outside the endowment. The university earned only $5 million in non-endowment investment income in 2015-16; that amount was $28 million in 2024-25. How is that income allocated within the university?

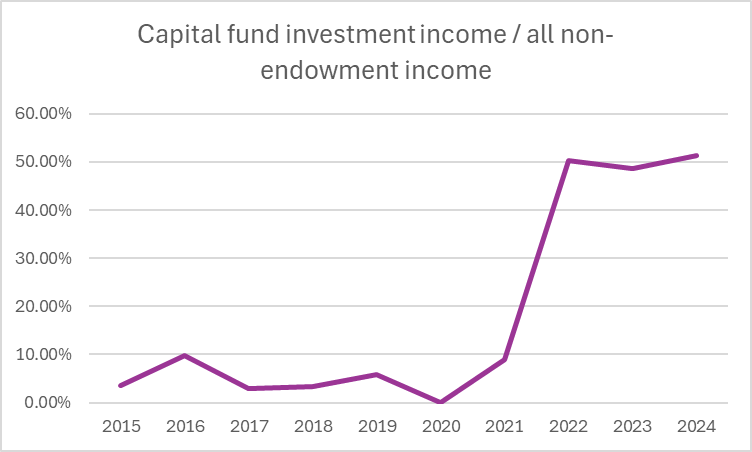

This is the third important change to investment income over the last ten years or, really, during the last three. There has been a massive jump in the portion of investment income designated as having been earned within, and allocated to, the capital fund. That trend is visible in the graph above. I’ve also put it in percentage terms below. The upshot is that an average of about 2% of non-endowment investment income was allocated to the capital fund between 2015 and 2020, while in the last three years, about 50% has been allocated to the capital fund. A cumulative $37 million in investment income was allocated to the capital fund over the last three years: $8 million in 2022-23, $14.5 million in 2023-24 and another $14.5 million in 2024-25.

There may be some perfectly reasonable explanation for this shift. I had considered for example that the change might be the result of payments from interest rate swaps that the university uses to hedge increases in payments on borrowing to finance capital projects. But that premise is not compatible with either the massive scale of the increase nor with the lack of corresponding adjustments in other parts of the budget reports. It dwarfs changes to the cost of financing.

If there is some consistent or principled rationale of the allocation of investment income, I have not been able to find it. There is no indication in the annual financial statements of how the allocation is being made. And while there are many university policies concerning the governance of endowment funds, there seem to be none that address how non-endowment investment income is to be allocated. Update: Dalhousie does have an Expendable Funds Investment Policy. It is primarily concerned with how cash balances will be invested, not how they will be allocated among funds. It does allow for some money to be invested in “internal loans.” But there is no evidence of a “loan” being made from expendable funds to the capital fund.

On the evidence I have, it appears that the allocation of non-endowment investment income between operations and capital is being done arbitrarily or, put differently, in accordance with the board’s assessment of strategies and priorities. It appears the board decided over the last three years to allocate $37 million to capital spending, rather than using (more of) that money to fund operational surpluses, build up carry forwards in academic units, and grow reserves. It appears that it decided in particular to allocate $14.5 million in investment revenues to the capital fund in 2024-25–while imposing a hiring freeze, pulling $3 million out of operational reserves, clawing back carry-forwards, and running a $6 million operational deficit.

I’ll finish with three hard questions:

How does the university decide how to allocate its non-endowment investment income? Is there an accounting rule or other policy dictating which fund will be designated as the source of that income?

If the amount of non-endowment investment income being allocated to the capital fund is more or less up to the discretion of the board, how much investment income is the university planning to allocate to the capital fund next year? Or over the next three years? Notably, $14.5 million per year looks pretty similar to the annual $17 million hole in revenue that is the starting point for the board’s operational budget plan for the next three years.

If the board made a strategic decision that it was necessary, rational or otherwise in the best interests of the university to spend half of the $70 million in financial windfalls earned over the last three years on capital improvements, on what basis was it decided that this capital spending would be accounted for as investment income earned and spent within the capital budget, rather than as investment income earned in operations and then transferred to the capital budget? Unless there is a good reason, the only conclusion I can imagine is that the board wanted to hide this income during budget consultations and mislead the university community about the actual amount and allocation of revenues available for operations rather than be open about the need for these investments.

Varia

September 18: Added “in” to “Recent annual financial reports attribute this jump to a rise in interest rates that…” Corrected “non-investment income” to “non-endowment investment income” Added an update addressing the Expendable Funds Investment Policy.

How much money does Dalhousie University have to give professors a raise? Three weeks ago I posted preliminary versions of two differentperspectives on that question. I’ve spent an embarrassing amount of time trying to answer some of the questions I raised in those threads. The result below sets out two broad and conflicting narratives, tests out critiques of each one, offers plausible explanations for holes in each account, and finishes with some broad conclusions. I mostly land with a focus on how much interpretive flexibility there is about the reality of budget constraint, though my reading has certainly narrowed the breadth of plausible estimates about how much budget flexibility there is.

Two caveats to start.

First, most of what I’ve said is based on the annual financial statements published by the university. While I think I’ve done a fair job interpreting those documents, I am not an expert. I teach business associations law and I’ve sat on a few non-profit boards, but I have no formal training in accounting. Nor, because of the lockout, have I been able to discuss my views with anyone at Dalhousie who could confirm or correct my understandings. Someone with more expertise might find errors in my reading (I’d be happy to hear corrections!). It may also be relevant that financial data I am relying on are published by the administration. The university accounts for its pools and sources of funds in obscure ways, and I am sympathetic to arguments that the obfuscation is deliberate. Nonetheless, given the layers of credentialed professionals involved in tracking, collating and reporting this financial data, my basic starting point is that these documents are accurate and reliable. My interest is in trying to make sense of what they say (and what they do not say). If you believe the university is lying, to the point that its published financial statements are untrustworthy, you are unlikely to find much of value in my attempt to interpret them.

Second, a word on my motives. The current round of bargaining between the board of Dalhousie University and the Dalhousie Faculty Association has been a bitter one. The board locked out faculty and other members of the bargaining unit on August 20. It is now September 11 and we do not feel close to a deal. As the days away from our work have stretched on, the choices made by the parties during the bargaining process, the lockout and on the picket line have bred frustration, recriminations and feelings of ill will. Many colleagues have lost faith in the administration, the union or both. One issue driving perceptions of poor judgement and bad faith is fundamental disagreement about the true state of the university’s finances. The administration claims they are facing significant revenue shortfalls that require drastic spending cuts. The union claims the university actually has money to spend and has other agendas. It feels like someone must be lying.

My aim here is not to say which interpretation is right. In fact, my basic conclusion is that, at least with data I have access to, there are many reasonable views of Dalhousie’s financial situation. Rather, my aim is to contribute in some small way to reducing the sense of indignation many of my colleagues feel about the actions of the administration or the union. That reconciliation requires a capacity to understand where each side was coming from. You may not find my justifications and glosses convincing. That’s okay. The point is just to be aware that some others might.

Somehow this has also ended up being 8000 words, so for the sake of convenience you can jump straight to the end if you’re not concerned with what’s happening under the hood. Now, off to the races.

Take 1: Cuts to Public Funding and Dalhousie’s Operational Budget Deficit

Every year the board approves and the university publishes an Operating Budget Plan for the upcoming year. In late summer, it reports Operating Budget Results against that budget in its annual financial statements. The administration’s bargaining position has been structured by the same story about the university’s finances they recounted during last year’s budget consultations. It’s the same story reflected in both the 2024-25 operational budget results, and in the 2025-26 Operational Budget Plan approved by the board. How does that story go?

In 2024-25, after a year with an imposed hiring freeze and the imposition of various austerity measures, Dalhousie reported a $6 million operational deficit, after transferring $3 million from “designated reserves”

Operating Budget Results from page 15 of the 2024-25 Annual Financial Statements

The shortfall the board is forecasting for the upcoming three years appears even more dire:

Over the next three years, the administration will allocate gradually less to academic and other units, asking them to eventually make do with spending 5% less than in 2024-25, in order to save a cumulative $46 million (label #1 in the image above). The budgeting reality for the various units is actually worse than this plan makes it appear, though. In contrast to prior practice, where the university set aside a portion of the budget every year to account for wage growth, the administration has told faculties that at least for the next three years they will have to absorb any compensation increases by finding savings or new revenue. Any rise in per capita salaries will have be made up by decreasing staff complements, finding other cost savings, or generating new revenue, meaning actual cuts to faculties and other units by 2027-28 are likely to feel more like 10-13% (depending, of course, on what kind of per capita raises are negotiated with various employee bargaining units). Notably, despite these projected cuts, the administration expects to run cumulative deficits of about $41 million (#2 above).1The budget plans indicates a cumulative $50.9 million deficit, but that includes the $9.8 milllion deficit already incurred in 2024-25

The gap between revenues and expenses has both immediate and structural causes. In accordance with this year’s funding deal, the provincial operating grant is projected to increase by only 2% per year over the next three years. Tuition revenues are expected to rise even less. There is no reasonable expectation that enrollment will increase. The province has frozen tuition for Nova Scotia students. And since the administration has decided not to introduce differential fees for out-of-province students, all undergraduate fees are frozen for the foreseeable future.2The 1-1.5% tuition revenue increases projected for each year are due to increases in tuition for international students and those in certain deregulated professional programs.

Structurally, the university’s financial woes can be attributed to the interplay of provincial and federal policy over the last ten years. While Nova Scotia’s block operating grant to Dalhousie rose in nominal terms from $187 to $203 million between 2014 and 2024, that constitutes as a 15% fall after accounting for inflation, even as provincial revenues rose in real terms by 20%. Dalhousie has increasingly relied on tuition fee revenue to make up the difference. Between 2014 and 2024, average undergraduate tuition fees in Nova Scotia climbed from $6483 to $9762 per student–a real increase of 17%. Dalhousie did even better than that. Unlike smaller institutions, it benefited from deregulated and steeply rising fees in professional programs like law, medicine and dentistry. Like many post-secondary institutions in Canada during the last ten years, it also employed a strategy of enrolling more international students, who pay much higher fees, to pad its revenues. The university also doubled its investment revenues, but the increase had a small absolute impact given that investment started as a relatively small portion of revenue. [Edit: the chart and discussion below does not take into account the $14 million in investment income that the university did not include in either the operational budget or operational budget report for 2024-25. That amount makes a big difference to the analysis.]

Compare Dalhousie’s core operational revenues in 2014-15 and 2024-2025:

Year

2014-15

2024-25

Provincial Grants

$213 million

$233 million

Tuition Fees

$141 million

$240 million

Investment

$26 million

$51 million

Total

$380 million

$524 million

The jump in total revenues from $380 to $524 million may feel like a windfall. Yet the headline number accounts neither for the significant inflation of the last ten years, nor for changes to enrollment. Dalhousie had about 18 800 full and part time students in 2014-15; it had 21 000 enrolled in 2024-25.3Dalhousie has historical enrollment data available online, but only going back to 2019. My enrollment numbers are taken from Association of Atlantic University data. Though total operational funding has increased from $20 200 to $24 900 per student over ten years, that’s a 5% fall in real terms.

The key issue is less the scale of the change over ten years than the recent trend. Between 2014 and 2022, Dalhousie’s operational revenues kept pace with inflation only because of steady increases in international student enrollments, rising from about 2700 to a peak of almost 4900. It was already clear in 2023 that those increases were unlikely to continue; in fact, international enrollments fell by 10%. Here is where federal policy comes in. With the major changes to immigration rules introduced by the Trudeau government in late 2023, international enrollments for 2024-25 fell across the county, and fell at Dalhousie in particular by an additional 20%.

This has had two implications for Dalhousie’s bottom line. On the one hand, the institution saw a one-time operational funding cut of $17 million in 2024-25. The bigger issue is that the strategy the university has pursued over the last decade to make up for gaps between increasing costs and decreasing public funding is no longer available. The university is facing a future in which existing revenue streams are expected to grow at only 1.5-2%, from a starting point where revenues are already 3% lower than in 2023. With many costs growing faster than 2%, the gap will only grow wider.

Take 1a: Financial Windfalls?

Before exploring the major alternative to this narrative, it’s worth addressing two points I’ve heard colleagues raise about the numbers in both last year’s budget and the projected budget plan.

As I elaborate below, the university’s audited financial statements tell a different story than the operating budget results reported in its annual financial statements. One aspect of the reports I found surprising is that endowments generated $76 million in investment returns, but Dalhousie only spent about $38 million of that.4page 37 of the 2024-25 Annual Financial Report, reproduced below. The university actually spent $43 million, but $5.4 million went to endowment management expenses. The remainder was reinvested. Over the last ten years, with gifts and reinvested returns, endowment assets have grown from $399 million to $753 million at the end of 2024-25.

Taking a closer look, though, this is roughly what you’d expect. The endowment allows the university to earn income from financial markets. Investment returns fluctuate a lot from year to year, and sometimes investments lose money. An organization that relies on endowment income to fund operations does not want to have a sudden and significant hit to its operating budget because of this unpredictability in market returns. That’s why, in line with standard expectations about long-term market returns and a goal of ensuring donors that endowed funds won’t be depleted, Dalhousie has an Endowment Fund Policy that commits the university to spending only 5% of endowment assets in any given year. The basic premise is that this will allow the fund to keep up with inflation, actually grow slightly over time, and provide consistent funding even when market returns are low. The $38 million allocated from the endowment to the operating budget in 2024-25 is slightly over 5% of the $700 million in the endowment at the beginning of the year.

I suppose the university could spend more when there is a windfall. What it cannot reasonably do, however, is budget for the future based on an assumption that financial returns will consistently average more than 5% over inflation.

Take 1b: A Diversion to Strategic Initiatives?

The more important line of critique concerns the over-$46 million the administration has budgeted in the next three years for “Strategic Initiatives and Essential Priorities.” (see #3 above) Between 2020 and 2024, the university spent about $5 million per year on this budget line.5$5.3 million in 2020-21; $4.1 million in 2021-22; $6.9 million in 2022-2023 and $4.8 million in 2023-24 In 2024-25, spending in this area was cut down to only $2 million.6See page 23 of the 2024-25 financials Under the current budget plan, the university plans to spend average of over $15 million per year over the next three years. Why is the administration tripling spending on special projects while asking academic units to cut annual spending by something like 10% by 2027-28?

The 2025 Operating Budget Plan gives some hint of how this money will be spent.7see page 6, 19, 29-30 Some money will be allocated to trying to improve enrollment and student retention (and thus grow revenues). Some will flow into faculty-level projects, possibly cushioning the blow of the cuts. This reflects an apparent shift away from unit spending autonomy toward more centralized budgeting (through the “integrated planning framework”). The university has stated their hope that the $27 million in planned cuts from academic and other units by 2027 will come through “administrative savings”–code for a familiar austerity agenda of having the same amount of work being done by fewer people. Some of the strategic initiatives spending will apparently be spent to develop systems and practices to facilitate this project of doing more with less. Read in the best light, then, this money will be dedicated to generating new revenues and identifying ways of reducing costs with minimal organizational consequences.

I don’t want to take a strong position here on the substance of these proposals. “Doing more with less” often translates to letting people go, not replacing retirees, and asking others to make up the shortfall. The Schulich School of Law currently lacks funds to replace most of the six or so faculty we’ve seen retire in the last two years. “Better systems” cannot make up for lacking faculty to teach core courses and advance research agendas. At other institutions, the implementation of new systems has meant a reduction in support staff, and a diversion of faculty time away from teaching and research into filling out paperwork through hard-to-learn digital interfaces. These points though, are about the cuts being planned, not the spending being committed to minimizing the pain of those cuts.

What I find most troubling about the strategic spending is that the scale of that planned spending exceeds the aggregate cuts that academic and other units are being asked to make. I am somewhat assuaged in my indignation about this allocation by the choice to offset much of the funding for these special initiatives through deficit spending. The intention seems to be to spend $45 million now, funded through $40 million in deficits, and hope that the money spent leads to a more sustainable budget, which can then be used to pay off the accumulated deficits in the medium term. The logic is of a short term investment that will (fingers crossed) generate positive long term returns.

Now, accepting this characterization of the strategic initiatives spending as deficit-financed investment, it is easy to critique how the various elements have been balanced together. Because the $45 million budgeted for strategic initiatives exceeds the planned deficit, it increases the amount of required cuts to unit spending by an aggregate $5 million. Does so much really need to be spent on these projects, so quickly? Could the university run slightly larger deficits in the short term, in order to delay the steep cuts to academic units? After all , if cuts to the university’s core mission are too steep, that could also harm the university in the long term; preventing steep cuts is itself a form of investment.

In part, the budget plan may reflect a project, one worth its own discussion, about the balance of spending authority and decision making between the academic units and central admin. Yet the budget plan also reflects a significant shortfall in future revenues no matter how you cut it. Take out the $46 million in special initiatives funding over the next three years and the administration would still be faced with cutting a cumulative $40 million from unit budgets, running a cumulative deficit of $40 million, or some combination of the two. That’s not sustainable in the long term.

Take 2: The Actual Budget

There is a more profound critique of the picture drawn of the financial situation laid out in the operating budget plan, though the longer I’ve spent with it, the less profound it has seemed.

What is odd about Dalhousie’s annual financial reports is that they set out two distinct pictures of the university’s financial life (along with a synthetic overview and analysis of trends of the university’s finances, explanations of variances, and various supplemental schedules). The first, the “Operating Budget Results,” reports revenues and expenses against the baseline created in the Operating Budget Plan approved by the board for the year. It is those budget results that show a $6 million deficit for 2024-25.

The other accounting of the university’s finances are found in the audited/consolidated financial statements. They provide a profoundly different picture of how the university is doing financially. Here is last year’s statement of revenue and expenses.

The results here diverge in various ways from the operational budget results. The biggest surprise, however, is that number at the bottom. While Dalhousie had an operational deficit of $6 million in 2024-25, it had an overall “excess of revenue over expenses,” i.e. a surplus, of $55 million.

When I first saw this number, I presumed it was an artifact of accounting methods, or a one-off product of reporting long-term financial flows in one-year chunks. So I looked through the audited financial statements for the last ten years. I’ll let the results speak for themselves:

Year

Net Income or Loss

2015-16

$20,585,00

2016-17

$23,502,000

2017-18

$33,080,000

2018-19

$41,012,000

2019-20

$48,878,000

2020-21

$61,810,000

2021-22

$67,378,000

2022-23

$76,922,000

2023-24

$55,719,000

2024-25

$54,945,000

Total

$463,246,000

Dalhousie has had an aggregate surplus of $463 million over the last ten years. When I first collated these numbers, that total did me a small amount of psychic damage. If the university is earning an annual surplus, why is it demanding steep spending cuts? How can the university claim to be in dire financial straits while it has made almost $500 million in “profits” over the last ten years? Where did the money come from? Where did that money go? Let me address those questions in turn.

Why the discrepancy?

Behind the scenes, Dalhousie uses a system of fund-based accounting. Internal budgeting and accounting processes designate revenue and expenses under six different funds, based on activity type: operations, endowment, ancillary, capital, special purpose, and research. Accounting for revenues and expenses in each fund is done almost as if those activities were done within a separate organization. If a cost is incurred in one fund that should properly be done in another, it is accounted for by transferring between the funds and then accounting for the cost or revenue where it belongs.8see page 29-30 of the 2024-25 Annual Financial Statements for further explanation and page 53 for revenues and expenses broken down by fund For example, the operational budget results for 2024-25 included $49 million in spending on campus renewal. In the fund-based accounting, that was accounted for as a transfer from the operations fund to the capital fund (as if university operations were paying rent to the capital fund), and then as money spent on construction and repair within the capital budget.

There are good reasons to budget this way. The operating fund comprises two thirds of all income and expenses every year and includes all the direct costs of employing professors and administrative staff, providing student services, paying scholarships and bursaries, funding travel, etc. The endowment is essentially an internal revenue source. Research (and special projects) funds need to be segregated to ensure they are spent in accordance with the rules and expectations of funders. Ancillary services–including housing, the Dalplex, food services, printing and parking, etc–are supposed to be revenue neutral. Accounting for those services separately makes it easier to ensure that operational funds are not subsidizing pay-for-use services, and that students and others aren’t being gouged in the university’s favour.

Fund based accounting also makes it easier to account for spending where the value of an expense is spread out over multiple years, which is the case for various forms of physical infrastructure (“capital”). The key to understanding the discrepancy between the operational budget results and audited financials is to appreciate how the university accounts for capital spending through the capital fund. The capital fund tracks the value of capital assets, net of debt and “deferred capital contributions.”

The debt is self-explanatory–it’s money the university has borrowed to finance capital projects. The nature of the capital assets and the set-off for deferred capital contributions both need some explanation.

The capital assets comprise the entirety of the university’s physical infrastructure: the land, buildings, books, equipment, vehicles, fixtures and software that everyone at the university uses to do our work. The capital assets are valued by summing the amounts initially paid for those goods or property, and subtracting amounts each year to account for depreciation (wear and tear), in accordance with a standard amortization schedule.9The amortization schedule is on page 41 of the 2024-25 Annual Financial Statements

What about “deferred capital contributions?” When the university receives a grant or gift intended to fund a capital project, it chooses not to account for that contribution as revenue in the year it receives the funds. Nor is the gift counted as revenue in the year the money is spent toward completing a project. Instead, once the physical asset is built, the contribution is accounted for as annual revenue amortized over the expected life of whatever infrastructure the gift or grant paid for.10see page 47 in the 2024-25 Annual Financial Statements Functionally, this practice seeks to smooth the measure of money contributed to help build or upgrade infrastructure over the life of the project the money is used to build. Not-yet-recognized deferred capital contributions have to be deducted from the value of the capital fund because the value of physical capital reflects the value of gifts and grants that have already been spent but will only be recognized as revenue in future years. 11Don’t worry, this hurts my brain, too. In future years, those capital contributions will be recognized as revenue, the offset will be reduced by the corresponding amount, and the value of the capital fund will increase.

Now back to the picture that includes all the funds. The formal reason the operational budget results differ from the audited financials is that the latter provides a comprehensive, consolidated picture of revenues and expenses across all six funds, while the former only aggregates accounting across operations, the endowment, and ancillary services (net of transfers to and from the other funds).

Why is the board’s annual oversight of the budget limited to approving an operational budget that only includes slightly over half of the university’s annual revenues? Why does the university’s budget advisory committee only consult with faculty, students and other stakeholders on the so-called operational budget? Why is the focus in annual reporting on the operational budget rather than the comprehensive financials?

There are two functional rationales to have annual budgeting focus on operational spending.

The first is that it offers a clearer picture of how the university is spending money. If an organization receives $1000 in a given year and immediately spends it buying library books then, in the aggregate, the university will enjoy a $1000 surplus. It received $1000 in cash as income, exchanged that $1000 in cash in return for $1000 in books, and ends the year $1000 (in books) richer. Operationally, though, the $1000 spent on books should be recorded as an expense, meaning the transactions are revenue neutral. Receiving and then spending the $1000 should create neither a surplus nor a deficit. Similarly, if the university receives $1000 and uses it pay off $1000 in debt, then that money is gone. But from a consolidated perspective, the university is better off by $1000, since its debt has been reduced by that amount. Fund segregation helps to make this clear. While in the consolidated financials, money received and then spent to pay off debt counts towards a surplus; at the fund level, it’s recorded as money being received by operations and then transferred to the capital fund, which will show a net increase of $1000 (net of any interest paid).

The other rationale for limiting the annual budgeting process to the operating budget is that the board does not have that much control in a given year over other parts of the budget. The amount of money that comes in for research, and how that money is spent, is mostly within the discretion of the academic staff. The university has a role in administering it, but no say in how much comes in and only minimal oversight over how it is directed. Nor does the university have much control in a given year about how much its stock of capital goods will cost in nominal or actual terms. There is no separate decision to make about “the capital budget.” Any interest on debt borrowed to finance a building has to be paid. The building itself falls in value every year because of wear and tear. It is important to include both amounts in an accurate accounting of all the university’s revenue and expenses. And yet, these amounts cannot be affected by budget decisions by the board at the beginning of the year.

This is not to ignore the significant role the board plays in shaping the university’s capital spending, nor the impact this spending has on the university’s operational budget. As for the board’s involvement, the university passed a Capital Projects Governance Policy in 2014. Under that policy, the board must not only to approve any capital projects undertaken by the university. They are also obligated to develop and approve a Multi-Year Capital Plan used to assess and evaluate each specific capital project. The board in short is heavily involved in approving new buildings, demolitions, major renovations and other major infrastructure projects–including an evaluation of how the construction and operation of those projects will be financed.

The board’s long-term decisions about capital spending also have significant implications for the operational budget. For one, operational revenues can be spent explicitly and directly on new capital projects. In the last eleven years, the university has done so exactly once, spending $300 000 on “capital investment” in 2023-24. Yet much of the university’s budgeted spending on “campus renewal” also adds to the capital fund by paying the costs of major renovations, additions, and upgrades to equipment, as well as paying off debt for prior construction. For much of the last eleven years, the operational amounts spent on campus renewal fell well short annual capital amortization (see chart below). Were it not for non-operational revenue for capital expenses, this would have meant a shrinking capital fund and a growing problem with deferred maintenance (think leaky roofs and broken fire sprinklers). Over the last eleven years, though, not only has capital amortization grown by close to 60% in lockstep with growth in the capital fund (see below), but operational spending on campus renewal has climbed, and now exceeds the amount of capital amortization for the last three fiscal years. Notably, the board’s 2025-26 budget plan includes spending on campus renewal for the next three years that grows about 2% per year despite how high it has already climbed.

Data is from Annual Financial Reports for 2014-15 to 2024-25. Campus renewal spending is taken from operational budget results; capital amortization is taken from the audited financials.

Where did the money go?

While this may clarify why the aggregate financials are different than the operational budget results, understanding how the university can run a deficit in one while running a surplus in the other requires attention both to where the surpluses have actually gone and where they came from.

Dalhousie is a non profit organization. It doesn’t have shareholders to pay off. No one has been made rich off of the annual surpluses. So where did it go? It became organizational equity–a surplus of assets over liabilities. Dalhousie’s net assets in March 2015 were $975 million. Over the next ten years that equity grew by $922 million, to reach $1.897 billion in March 2025.

Net assets, 2014-15 (in $thousands)

Net Assets, 2024-25 (in $thousands)

How could net assets have increased by $922 million if aggregate surpluses were only $463 million?

As background, it’s important to understand that the administration does not actually segregate assets and liabilities among the six funds discussed above. There is no pile of money and investments called “the endowment.” Instead, the university has assets in various forms–property and equipment, cash and investments, accounts receivable. Those assets are subject to various liabilities and quasi-liabilities: actual debts to repay, accounts payable, resources that have been received but must be spent for a specific purpose. This is why it’s important not to give too much attention just to how much the university currently holds in cash (ahem). The net assets, or equity, which is the difference between assets and liabilities, are accounted for in four broad categories: endowment, pension surplus, the capital fund, and the catch-all “restricted funds.”12see page 35 of the 2024-25 Annual Financial Statements

The explanation of the gap between the surplus and the growth in equity is that two of these asset categories are included in net assets but excluded from accounting for revenues and expenses. $350 million of the increased equity is attributable to growth in the endowment fund. As discussed above, when endowment income is spent in a given year, it counts as revenue, but in light of the commitment to maintain the value of the fund, the reinvested amounts are not treated as revenue at all. It’s as if the endowment revenue comes from an external funder.

Another $100 million of the increase in net assets comes from a swing in the balance between the university’s present pension assets and its future pension liabilities, from a $9 million deficit in 2015 to a $92 million surplus in 2025. Changes in net pension liabilities are also excluded from calculations of annual revenues and losses. This is sensible. The fund regularly swings between surplus and deficit, and the current surpluses may be gone in a couple of years. That does not mean that fluctuations in the value of pension assets are irrelevant to the university’s finances. The current surplus does benefit the university’s bottom line, by reducing their employer contributions, on the order of $3 million per year. But given the regular swings between surplus and deficit, that savings is neither predictable or reliable. (Given that the real question of interest is whether the university has operational wiggle room, it should be noted that this $3 million per year is already included in its budget forecasts.)

When you take away the changes to the endowment and the pension, the remaining $472 million increase in equity corresponds almost exactly to the $463 million in net budget surpluses over the last two years. Those surpluses have increased the value of net assets in two fund categories: there has been a $116 million increase in “restricted funds” (from $91 million to $207 million), and a $349 million rise (from $395 million to $844 million) in the capital fund.

Let me start with the capital fund. Comparing the 2014-15 and 2024-25 financials, you can pull out the major contributors to the increase in the value of the capital fund:13The differences are calculated from a comparison of data in explanatory notes 5 and 12(d) from the 2015 financials with data from notes 5 and 11(e) from the 2025 audited financials

Contributing factor

Amount

Buildings

$348,948,000

Capital reserves

$25,471,000

Equipment

$26,189,000

Working capital

$19,594,000

Deferred capital contributions offset

(-77,624,000)

There are a few other numbers in the mix but, once you get down to the carpet tacks, three quarters of the $463 million in budget surpluses earned over the last ten years have gone toward growing the capital fund, and the entirety of that growth is the result of money spent on either new buildings or major renovations to existing ones.

Is this scale of investment in buildings reasonable? That $348 million investment amounts to a 54% increase in the value of Dalhousie’s plant and infrastructure, or 5.4% per year. Okay, but recall the enrollment growth discussed above. It’s still a 38% increase on a per student basis. Perhaps it’s not enough though to just maintain buildings and add a few new seats. Perhaps there are good reasons to want the university’s infrastructure to improve so that its value rises with inflation: to create infrastructure that is attractive to students and faculty (and donors), to keep up with technological developments, to or meet new building code requirements or sustainability standards. In real dollars term, on a per student basis, that $348 million is only a 7.5% increase over ten years. Can that 7.5% increase be justified? Maybe. Consider, for example, that the university has also increased its research intensity, with revenues rising 80% over the last ten years.

What about the “restricted funds?” These restricted funds are not money received but not yet spent on research, special projects, or operations and ancillaries. Those amounts are designated as “deferred revenue” and count as a liability in the calculation of net assets.14See page 35 and explanatory note 7 on page 44 of the 2024-25 Annual Financial Report. Nonetheless, some of these restricted funds are apparently unspent contributions from external sources that have narrow, specified uses. The vast majority (about $189 million) are “internally restricted funds,”15page 37 of the 2024-25 Annual Financial Report which the financial statements describe as “amounts set aside … for specific uses including unspent budget appropriations accumulated by academic and other budget units, operating surpluses from prior years, certain fundraising activities and including departmental research overhead and development funds.”16page 48 of the of the 2024-25 Annual Financial Report

How are these funds split among these uses? Dalhousie has long followed a policy of not recouping unspent funds from faculties and other units every year. If a unit does not spend amounts allocated to it by the university, the university reserves that amount as a carryover that can be used to defray the unit’s budget overruns in future years. That money is treated as spent in the operational budget results, but unspent in the consolidated financials. Over the last ten years, academic and other units have accumulated close to $87 million in net carryovers. Academic units alone are entitled to $27 million in accumulated carryovers.17My calculations, based on Schedule 2 of the consolidated financials from the 2015-16 to 2024-25 Annual Financial Statements. On the other hand, even including recent deficits, the university’s cumulative operating surpluses over the last ten years have been about $18 million.18My calculations. Those two increases together explain $105 million of the $116 million increase in restricted funds. That leaves only $11 million of the ten year surplus unaccounted for.

Where did the money come from?

Figuring out the sources of the surplus is tricky. The discussion of “restricted funds” above makes clear that most the money came from under spending either at the unit level (cumulative carryovers) or at the university level (operational surpluses).

Figuring out how Dalhousie paid for the increase in the capital fund is somewhat more of a challenge. Recall what needs to be explained: the capital fund grew by $349 million over the last ten years. Net deprecation during that period was $446 million, which needed to be recouped for the fund to grow. So where did the $795 million come from?

As discussed above, $331 million came from the operational budget spending on “campus renewal” between 2015 and 2025.

The consolidated financials for every year include a recognition of revenue for “deferred capital contributions.”19See e.g. the line “Amortization of deferred capital contributions” on page 36 of the 2024-25 Annual Financial Statements As discussed above, this is not really new revenue, but simply a recognition of a portion of gifts and contributions made to capital projects that were already completed. In aggregate, these gifts, grants and donations to capital projects account for $167 million or so of the ten-year aggregate surplus.

Recall from above that ancillary services are supposed to be revenue neutral. Users of housing, parking, food services, etc are neither supposed to subsidize operations, nor vice versa. While there is intended to be no contribution between these services and the operational budget, the ancillary budget does have a net impact on the consolidated financials. In particular, their balanced budget includes a transfer to the capital fund, that intended to be equivalent to rent. Cumulative contributions from ancillary services to the capital fund over the last ten years were $131 million.20My calculations, based on “Ancillary–interfund transfers” from Schedule 1 of the consolidated financial statements

There has also been a significant revenue generated within the capital fund itself, including smaller gifts, and in recent years, investment returns credited to the capital fund. Aggregate revenue within the capital fund between 2015 and 2025 were another $77 million.21My calculations, based on capital fund revenue from Schedule 1 of the consolidated financials. I have excluded insurance proceeds in the 2019, 2020 and 2021 reports because they paid for expenses to repair fire damage. [Edit: As elaborated in a subsequent post, it is not clear how the capital fund generated so much in income and especially why $37 million in investment income was credited to the capital fund over the last three years.]

Together, those amounts explain $709 million of the $795 million that has helped grow the capital fund over the last ten years. My sense is these numbers get us most of the way there. Additional amounts are attributable to additional transfers from the research or special projects budgets.

The Upshot

What to make of all this? Recall the starting point: because of a major one-time fall in operational revenue and poor prospects for revenue growth, the operational budget plan for the next three years includes unit-level spending cuts that will ramp up to a 5% decrease plus the impact of absorbing any compensation increase, $45 million in additional spending on strategic initiatives, and an aggregate deficit of $40 million.

It might be best summarize my key takeaways from the above as a FAQ, focusing in turn on the revenue equation, the allocation of cuts, and whether there are resources to reduce their impact.

Is the board’s narrative about Dalhouise’s revenues constraints true? Yes, Dalhousie’s narrative about its revenue constraints are accurate. As a result of long-term underfunding by the province and a shift in federal immigration policy that collapsed international enrollments, Dalhousie’s operational revenues fell by $17 million between the 2023 and 2024 fiscal years. Projected revenues are only expected to grow by 1.5% per year. The university is exploring new revenue streams and encouraging academic units to do the same. Some would like to see our admin, or the post-secondary sector as a whole, advocate more vocally for a reversal of the significant government funding that are at the root of revenue issues in the sector. Update as of September 18: I am no longer sure that the board’s account of revenues is true, given the apparent under-reporting of investment income.

What about that $55 million surplus? Doesn’t that mean Dalhousie has more money to spend on operations? As well as operational budget results, Dalhousie publishes consolidated and audited financial statements every year. As reported in the latter, Dalhousie did have a surplus of $55 million last year. In fact, while net operational surpluses over the last ten years have been only $18 million, the university’s cumulative consolidated surpluses over the same period were an additional $445 million. Those surpluses, however, do not represent the diversion of revenues available for operations. Of that surplus, $87 million is reserved for unit-level budget carryovers from the past ten years, of which $27 million is held by academic units. This money represents spending that was allocated in annual operating budgets but not actually spent by the units to which is was allocated. From the perspective of the operational budget, it was spent; it is now up to the unit to decide how it is allocated, not the board. But from the perspective of the consolidated financials, the university as a whole still has the money–leaving a surplus. The majority of the consolidated surplus, however–$349 million–is the result of spending on the university’s capital assets. When money was spent, it stayed on the books as an asset. It’s now in the form of new buildings, renovations and upgrades to old buildings, along with new library books and lab equipment. That $349 million, plus another $446 million to offset capital depreciation, came from grants and gifts, contributions from research awards and special project funding, rent paid for student housing and by other ancillary services–along with $331 million in operational funds spent on “campus renewal.”

Has Dalhousie spent too much on new and upgraded buildings? Maybe! Spending on capital projects over the last ten years has increased the value of capital assets by 54%. Even if you account for inflation and increases in enrollment, it’s still a 7.5% increase. Maybe capital was cheap and it was a good idea to build up when we could. Maybe we needed different, better buildings to fulfill our increased research intensity. Or maybe the board over-invested in unnecessary builds and upgrades, and the result will be increasing cost pressures on the operational budget. The question of whether this money was well allocated, however, is somewhat separate from what to do about the budget going forward.

Does the operational budget pay for capital improvements? Absolutely. Over the last ten years, the operational budget has allocated $331 million to “campus renewal.” All of this spending goes directly into funding renovations and upgrades, or to paying off debt that was used to finance recent capital projects. I cannot tell whether operational funding is explicitly used to support new buildings, but it makes little difference. In some sense, all of the university’s spending on capital projects helps support the continued growth of the capital fund.

Will the new hockey arena divert funds from academic budgets? I haven’t taken a look at the planning documents for the project, but everything I’ve seen in the university’s budgeting norms suggests the arena will fall under the ancillary budget, which means its operational revenues will be expected to cover the cost both of its ongoing operations and its original building costs. Of course, the project plan may end being faulty, leading to cost overruns, but as a matter of budgeting policy it is not supposed to have any impact on the operational budget. Update of September 14: Apparently, the university did spend $1.75 million on the arena out of an operating surplus in 2022. Even though the amount is small, I find this willy-nilly crossing of income streams problematic given my understanding of how fund segregation is supposed to work.

Can cuts be made in other parts of the operational budget instead of to academic units? Maybe in part! The university is planning to spend an unprecedented amount on “strategic initiatives” over the next three years. The cumulative $45 million in planned spending exceeds the $40 million or so in cumulative cuts that are planned for unit-level spending. The budget plan sets out some idea of how these funds will be used, but there is room for wide disagreement about whether that spending makes sense. Overall, however, even without the strategic initiatives spending, over the next three years the university would still be looking at running a $40 million deficit, making a cumulative $40 million in cuts, or some combination of the two.

What about cuts to operational spending on capital projects? Yeah, that might make sense. Over the last ten years, operational spending on capital projects, i.e. “campus renewal,” has increased by 92%. Under the budget plan, it will continue to increase by approximately 2% per year. In 2015-16, operational spending on campus renewal covered only 76% of all capital depreciation costs. Over the last three years, it has covered more than 100% of the cost of depreciation for all capital goods, whether dedicated to academic uses or not. While I can come up with reasons why the cost of building upkeep and upgrading has increased compared to the last ten years, it is not clear so much money needs to continue to be spent on capital projects. Does the board plan to continue growing the university capital stock by close to 6% a year? What would the consequences be, for deferred maintenance or otherwise, of reducing spending on campus renewal by $5 or $10 million per year? Such reductions may not be sustainable in the long term, but it could limit the impact of cuts in the short term.

Doesn’t the university have lots of money to spend? They have $400 million in cash, right? The key question is not how much cash the university has to spend but how much it has in assets neither burdened by liabilities nor reserved for particular uses. The university’s least burdened assets amount to about $207 million in “internally restricted funds.” At least $87 million of that is in faculty and unit-level budget carryovers from past years. The university may have as much as $120 million in a rainy day fund, though data from the last ten years would suggest it is much less. That said, given the administration plans to run $40 million in deficits over the next three years, that money won’t last very long without a change in the budget trajectory.

Are there other funds available that can cushion the blow of the cuts? Sure. As noted above, the university has at least $87 million in accumulated carryovers reserved for use by various units. At least $27 million is reserved for academic units. Some academic units may be able to spend this money to defray the impact of reduced allocations from the central budget over the next three years, but that will at best delay even steeper future cuts.

What about funding early retirement packages for high-paid academics? What about paying high-level administrators less? Don’t we spend too much on administration anyway? Maybe! But these are all questions about how operational cuts should be allocated among and within units. None of these ideas challenge the basic calculus of the budget projections.

Overall, where I’ve come to is that there probably is enough financial wiggle room to make it through the next three years without the drastic cuts forecast in the budget plan. That said, the university is starting off with a $17 million per year gap between revenues and expenses and unless we can find new revenues that gap will only grow with time. The university may be able to weather that shortfall through spending down accumulated surpluses and unit-level carryovers. It may be able to delay the cuts by reducing capital spending and deferring maintenance costs in the medium term. Doing so though is only delaying a reckoning.

Varia:

September 14: corrected various typos, added one footnote and deleted two orphaned and redundant paragraphs from immediately before the last section.Also added a note on the $1.75 million that was spent out of operating funds on the arena in 2022.

September 18: added numerous updates reflecting how the apparently hidden investment income amends my analysis. Moved the sentence “Functionally, though this amounts to a smoothed measure of the money that has been contributed expressly to help build or upgrade infrastructure” from the section “Where did the money come from” to the initial discussion of deferred capital contributions in the section “Why the discrepancy” and amended it to read “Functionally, this practice seeks to smooth the measure of money contributed to help build or upgrade infrastructure over the life of the project the money is used to build.”Added the sentence “Some academic units may be able to spend this money to defray the impact of reduced allocations from the central budget over the next three years, but that will at best delay even steeper future cuts” to the conclusion.

1

The budget plans indicates a cumulative $50.9 million deficit, but that includes the $9.8 milllion deficit already incurred in 2024-25

2

The 1-1.5% tuition revenue increases projected for each year are due to increases in tuition for international students and those in certain deregulated professional programs.

page 37 of the 2024-25 Annual Financial Report, reproduced below. The university actually spent $43 million, but $5.4 million went to endowment management expenses.

5

$5.3 million in 2020-21; $4.1 million in 2021-22; $6.9 million in 2022-2023 and $4.8 million in 2023-24

The amortization schedule is on page 41 of the 2024-25 Annual Financial Statements

10

see page 47 in the 2024-25 Annual Financial Statements

11

Don’t worry, this hurts my brain, too.

12

see page 35 of the 2024-25 Annual Financial Statements

13

The differences are calculated from a comparison of data in explanatory notes 5 and 12(d) from the 2015 financials with data from notes 5 and 11(e) from the 2025 audited financials

14

See page 35 and explanatory note 7 on page 44 of the 2024-25 Annual Financial Report.

My calculations, based on Schedule 2 of the consolidated financials from the 2015-16 to 2024-25 Annual Financial Statements.

18

My calculations.

19

See e.g. the line “Amortization of deferred capital contributions” on page 36 of the 2024-25 Annual Financial Statements

20

My calculations, based on “Ancillary–interfund transfers” from Schedule 1 of the consolidated financial statements

21

My calculations, based on capital fund revenue from Schedule 1 of the consolidated financials. I have excluded insurance proceeds in the 2019, 2020 and 2021 reports because they paid for expenses to repair fire damage.